Many UniCredit customers in Italy want a simple card for everyday payments, online shopping, and trips abroad, without dealing with credit checks or revolving balances.

The UniCredit MyOne Mastercard fits that role as an international debit card tied directly to your current account, available in both physical and digital form.

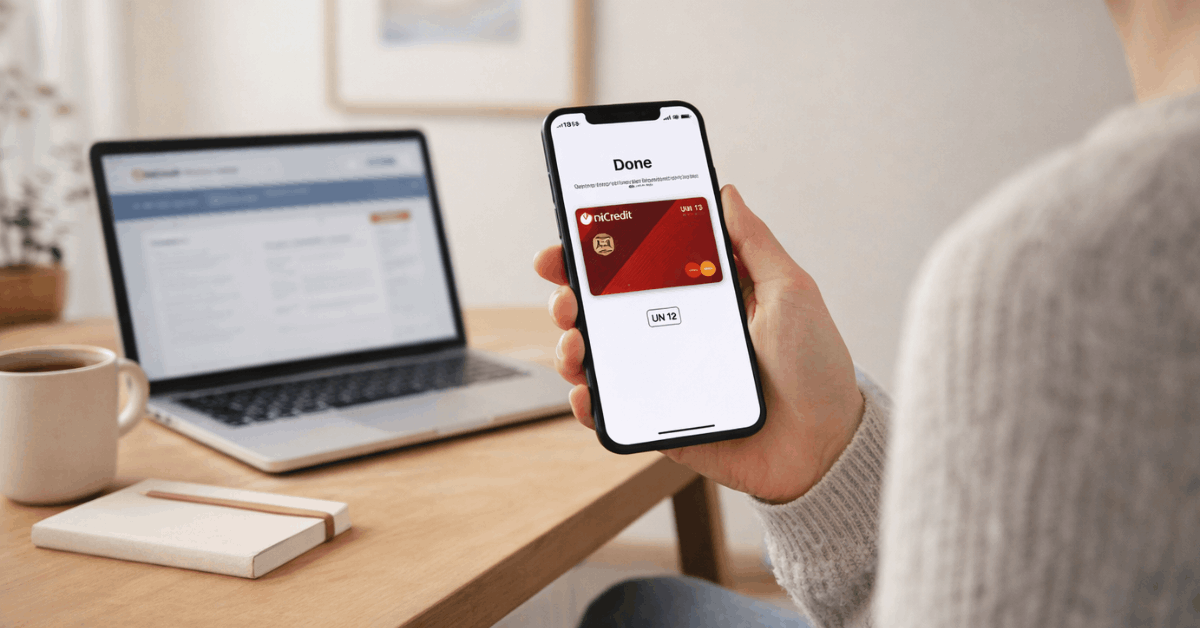

Focus stays on practical features: contactless payments in Italy and overseas, mobile wallet support, and security tools that keep online purchases under control. Anyone searching for a straightforward UniCredit MyOne Mastercard guide on how to request it online will find the process shorter than expected.

What The UniCredit MyOne Mastercard Offers

MyOne is an international UniCredit debit card issued on the Mastercard or Visa network and reserved for account holders of the bank.

According to UniCredit’s official product documents, it works for point-of-sale payments, ATM withdrawals, and secure online purchases in Italy and abroad. Daily shopping is faster with contactless payments at enabled terminals, while chip and PIN remain available when higher security is required.

Physical Card or Digital Version

Cardholders can choose a physical card, a digital version, or both, so a virtual debit card can be added to a smartphone wallet even before the plastic arrives. Key MyOne Mastercard features include support for Apple Pay and Google Pay, customisable limits, and 3D Secure protection on participating websites.

International Mastercard acceptance across millions of merchants helps your card stay usable on city breaks and business trips, provided the account holds enough funds.

According to external comparison sites that track Italian debit offers, MyOne sits among UniCredit’s main everyday cards, alongside other products on different circuits.

Costs, Limits, and Basic Conditions

According to UniCredit’s Italian pricing sheet, MyOne has an annual fee of 22 euros, plus 3.50 euros for issuing the card and 3.50 euros for shipping. Cash withdrawals at UniCredit ATMs in Italy and across much of Europe are free, while prelievi at other banks’ ATMs generally cost 2 euros per operation.

For withdrawals outside the euro area, a 2 euro fee applies plus a 1.75 percent markup on the converted amount, reflecting the use of international schemes.

Eligibility

Eligibility normally requires a UniCredit current account in your name, including accounts opened via digital branches such as Filiale buddy.

Age requirements and KYC checks follow Italian banking rules around identification, codice fiscale, and proof of residence.

PIN changes are flexible because UniCredit allows free modification once, then applies a small fee for subsequent changes. Those conditions can evolve over time, so checking the latest “Documenti Informativi” or speaking to the bank helps avoid surprises.

How To Apply For The UniCredit MyOne Mastercard Online

Most people prefer to request the card directly through digital channels rather than visiting a branch.

The online process sits inside UniCredit online banking and the Mobile Banking app, and usually takes only a few minutes when your documents and Banca Multicanale access are already set up.

A digital card can become usable almost immediately for e-commerce and wallet payments, while the physical card arrives later by post. Following the right order of steps reduces delays and avoids repeating identity checks.

- Access the UniCredit Mobile Banking app or log in to desktop UniCredit online banking using your existing multichannel credentials.

- Open the section dedicated to cards and select the option to request a new debit product, then choose the MyOne label when presented.

- Decide whether the request should create a physical card, a digital-only version, or both, keeping in mind that virtual issuance tends to be immediate.

- Review the economic conditions, set any initial limits, and sign the contract electronically inside the app using the standard digital signature workflow.

- Activate the card once the plastic arrives, either through the Mobile Banking area, internet banking, or the telephone banking service, then complete a first purchase or ATM operation where needed.

Current non-customers can usually open a current account and apply for MyOne in a single remote journey that includes a selfie video and online document upload for identification.

According to UniCredit’s own descriptions of its mobile onboarding, that remote flow replaces the classic paper contract and speeds up access compared to booking a branch appointment to apply for MyOne online.

Other Ways To Request The Card

Some people still prefer face-to-face help, especially when opening their first current account or switching banks. UniCredit allows MyOne requests to be made directly in a branch, where staff can open the account, collect identification documents, and submit the card application on your behalf.

That route suits customers who want to discuss alternative cards, overdrafts, or additional services such as insurance or investment products at the same time.

Another option involves using a smartphone to start the account opening process as a new client, then finalising the MyOne request in the Mobile Banking app after activation.

Paying, Withdrawing, and Managing Security

Every day spending becomes easier because MyOne supports contactless payments in Italy and abroad at terminals showing the appropriate logos.

Italian rules currently allow low-value contactless purchases up to 50 euros without PIN entry, as long as the cumulative total since the last PIN does not exceed 150 euros; once that threshold is crossed, the terminal requests authentication again.

Online transactions benefit from 3D Secure, which adds an extra one-time verification step or app notification to confirm that the operation really comes from you.

Card Management Using Mobile Banking

Card management happens largely inside Mobile Banking, where you can change PIN, adjust spending limits, and temporarily block or unblock the card in case of doubt.

According to UniCredit’s FAQs, loss or suspected misuse can be handled through the classic toll-free assistance number or via the “Problemi Carta” and “Gestione Carta” sections in digital channels.

Additional protection often comes from insurance coverage branded as “Protezione prelievi”, provided by CHUBB European Group SE and reserved for debit cardholders who meet the conditions.

MyOne Debit Versus UniCredit Credit Cards

Confusion sometimes appears because UniCredit also issues several Mastercard credit cards, such as Gold, Platinum, and Blue, that work very differently from a MyOne debit.

Foreign documentation for UniCredit Hungary, for example, shows Gold, Platinum, and Blue credit cards with credit lines between roughly 280,000 and 5,000,000 forint, annual percentage rates around 37 to 39 percent, and international travel insurance bundled as part of the package.

Those products often participate in cashback schemes and discount programs like Card+ and require at least five percent of the outstanding balance to be repaid every month.

MyOne is Different from the Rest

MyOne does not behave like those revolving credit lines, because every transaction immediately uses money held in your current account.

Interest on purchases does not appear, there is no separate credit limit to manage, and repayment schedules do not exist beyond keeping your account in the black.

That structure makes MyOne more suitable as a daily spending tool, while UniCredit’s credit cards target people comfortable managing debt, minimum payments, and promotional cashback programs.

Practical Tips For Using MyOne Safely

Day-to-day habits contribute more to safety and control than any single feature on the card. Short, consistent routines can keep the UniCredit MyOne Mastercard aligned with your budget and reduce risk when travelling or shopping online.

- Check your balance and recent movements in the app before large card payments, especially ahead of holidays or big sales periods.

- Enable transaction alerts in Mobile Banking so every purchase or ATM withdrawal triggers a push notification on your phone.

- Set conservative limits on ATM withdrawals, online spending, and contactless payments, then raise them temporarily when higher use is expected.

- Keep the physical card separate from documents that show your address, and avoid writing the PIN anywhere that could be found together with the card.

- Contact customer support immediately and use the digital block functions if the card goes missing or unfamiliar transactions appear in your history.

Last Thoughts

MyOne works best as a straightforward debit for daily payments, travel, and online shopping. Set clear limits in the app, prefer contactless and wallets, and watch balances ahead of trips.

Enable real-time alerts, block the card on doubt, and contact support immediately for issues. Confirm current fees, ATM charges, and shipping or issuance terms in UniCredit materials before requesting.

Disclaimer

This site provides general information on credit cards and payment products, not financial, legal, or tax advice; always verify rates, fees, and terms with the issuing bank before applying.