AI Credit Score Check tools are showing up inside lender apps, fintech wallets, and even “pre-qualify” screens. The idea sounds simple: pull a wider set of signals than a classic bureau-only score, then estimate creditworthiness faster.

That matters because a huge share of adults still sit outside formal finance, and even many account holders stay “unscorable” under older scorecard rules. World Bank Global Findex reporting puts the unbanked figure around 1.4 billion adults as of 2021, so smarter models keep getting attention.

Credit scoring still asks the same two questions: can the borrower repay, and will the borrower repay. Modern models simply try to answer those questions using more data and tighter statistical fit.

What An AI Credit Score Check Really Means

“AI credit score” usually means machine learning credit scoring that predicts repayment risk using patterns learned from large datasets. Traditional scoring leans on static variables and long credit histories, which blocks people with a thin credit file or no bureau record.

AI systems can evaluate broader inputs, then update decisions as fresh information arrives. A single score rarely tells the full story. Many tools generate a probability-style output, a risk band, or an internal grade.

Some lenders also convert ML outputs back into familiar scorecards so risk teams can review drivers in a format that looks like traditional underwriting.

What Data Usually Shapes The Result

More data does not automatically mean better decisions. Quality, consent, and relevance matter more than volume, especially under privacy rules and credit reporting laws.

AI models often combine traditional and non-traditional signals to estimate credit risk prediction:

- Income and stability signals: pay frequency, employer consistency, or verified income deposits.

- Payment behavior: on-time utilities, rent records where reporting is available, and bill-payment patterns.

- Bank transaction analysis: cash flow, spending volatility, and recurring obligations.

- Product and channel behavior: account tenure, overdraft frequency, and repayment timing.

- Fraud and identity integrity: abnormal device or login patterns, mainly for fraud detection rather than pricing.

This is where alternative data credit scoring shows up. Some systems use digital footprints or device metadata, but only under explicit consent and local legal limits.

How AI Scoring Works Behind The Scenes

Three mechanics drive most systems:

- training,

- prediction, and

- monitoring.

Training means feeding historical outcomes into a model so it learns which patterns tend to precede repayment or default. Prediction happens when an application arrives and the model scores that profile against learned patterns. Monitoring checks performance over time because populations drift and economic conditions change.

A useful mental model is real-time cash flow analysis. Rather than reading a single monthly snapshot, a lender might study income trends, expense consistency, and how often the account dips near zero. That approach can help applicants who earn reliably but never used credit products long enough to generate a robust bureau record.

Continuous learning is the headline advantage, but it carries risk. Updates must be governed so a model does not “learn” harmful bias or degrade silently during a downturn.

Where AI Beats Traditional Credit Scoring

Older scorecards can work well inside stable, mature credit markets. Problems appear when applicants lack long credit histories or when the scorecard no longer matches the current population.

Financial Inclusion is the Obvious Benefit

World Bank reporting shows account ownership has expanded substantially, yet 1.4 billion adults remained unbanked in 2021, and many more sit underbanked or credit-invisible.

AI-based models can help lenders evaluate applicants who would otherwise be rejected due to missing history. Industry examples point to that direction.

Upstart has publicly reported results from internal comparisons between its AI model and more traditional underwriting approaches, including higher approvals and different APR outcomes, while emphasizing model governance and risk controls.

Speed is the Second Advantage

Digital-first lenders can score in minutes, which fits modern onboarding expectations and reduces manual review queues.

Adaptability is the Third Advantage

When drift happens, monitoring flags it, and model refresh cycles can be quicker than rewriting a full scorecard strategy.

The Hard Parts: Black Box Risk, Bias, and Privacy

Explainability remains the biggest trust hurdle. Complex models can feel like a black box, especially when a declined applicant wants clear reasons. Regulators and industry groups keep pushing “explainable” approaches so decisions can be defended.

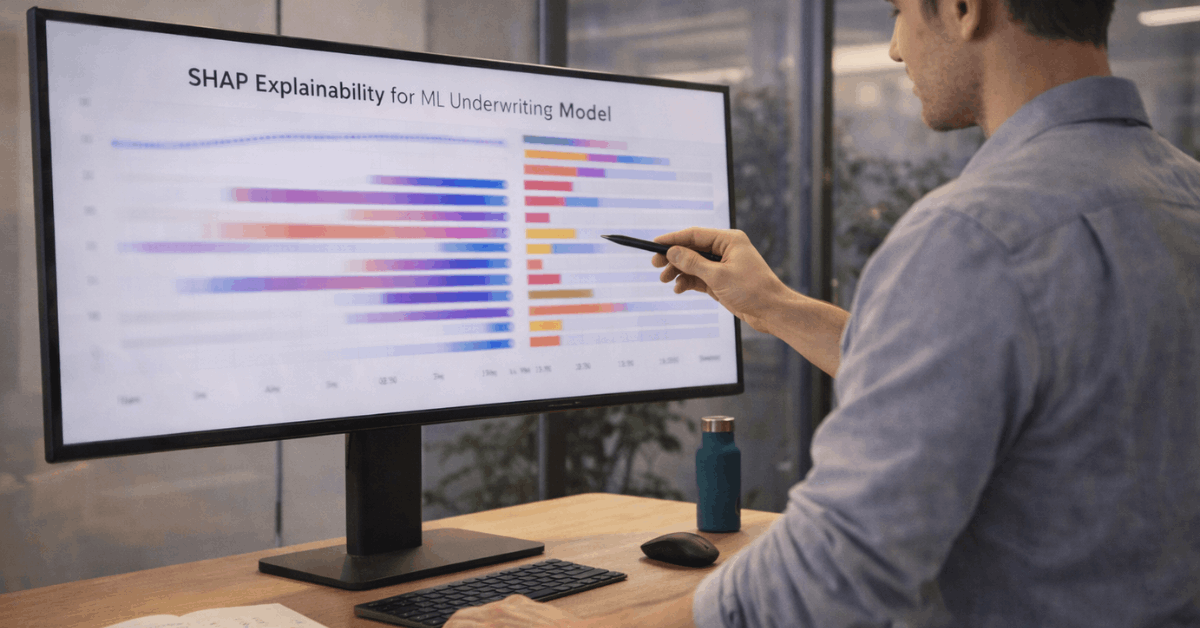

Feature Attribution techniques

One common method is explainable AI in lending through feature attribution techniques. The Bank for International Settlements has discussed SHAP as a way to show how specific features contribute to a credit underwriting output.

Those SHAP-style explanations often appear as color-coded impact plots or step-by-step contribution visuals that start from a baseline prediction and move upward or downward.

Bias Mitigation in Credit Models

Bias mitigation in credit models is the other serious challenge. Bias can enter through skewed training data, proxy variables, or uneven data availability across regions. Strong programs use audits, stratified modeling strategies, manual weighting controls where justified, and ongoing fairness checks.

Legal frameworks also shape what’s allowed. US markets often reference the Fair Credit Reporting Act and Equal Credit Opportunity Act, while many other regions focus on GDPR-style consent and purpose limitation. Local rules vary, so global products typically build guardrails for the strictest environments.

Privacy risk deserves equal weight. Alternative inputs should be consent-based, clearly disclosed, and limited to what is relevant for underwriting and fraud prevention. “More data” without a purpose map becomes a liability fast.

Reading Your Results Without Overreacting

An AI profile output usually signals drivers rather than destiny. Lenders may highlight issues such as income instability, high utilization, excessive short-term borrowing, or risky repayment timing.

Some tools also show scenarios: paying down a card balance, extending tenure, or reducing late payments, then estimating how those moves could shift the score band.

Practical interpretation stays grounded in the fundamentals. Debt-to-income pressure, repayment history, and cash flow volatility typically matter regardless of model type. A low score from one lender does not mean universal rejection, since features, weights, and risk appetites differ.

Safer Ways To Use An AI Credit Score Check

No single tool should run your financial life. Still, a clean process can turn results into better decisions and fewer surprises.

- Review permission screens and data-sharing settings before linking accounts.

- Compare bureau-based results and AI-driven results to spot mismatches.

- Treat explanations as priorities, then fix one variable at a time.

- Document changes for 30 to 90 days, then re-check trends.

- Stop using tools that cannot explain what data they collect and why.

A smart takeaway is this: the score is an output, the habits and constraints behind it are the real levers.

Last Thoughts

Treat AI credit score checks as decision aids rather than verdicts that define eligibility. Confirm permissions, read explanations, and focus on one fixable driver at a time.

Pay on schedule, lower revolving balances, and build stable income signals across months. Re-run the assessment after consistent changes, then apply where terms match your budget.